5 tips to successfully implement blockchain for businesses

When implementing blockchain, organizations should consider what problem they're trying to solve and how blockchain technology will add lasting value.

By

Paul Brody

Published: 17 May 2023

Learning how to implement blockchain requires a clear understanding of the technology's decentralized ecosystem.

Following these tips will help simplify your approach while providing quality ROI and the best results from a blockchain implementation.

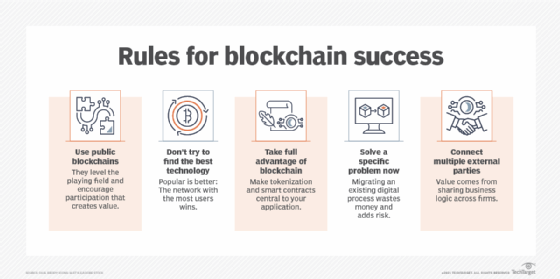

1. Real blockchain developers play with their tokens in public

Blockchains are decentralized ecosystems, so no one party controls the network as a whole and everyone participates with the same set of rules. Public blockchains, specifically Ethereum, are the only blockchains where this is the case.

Private blockchains look like blockchains on the surface, but they are controlled networks, and they haven't been as successful because users are wary of a system where the controlling entity can change the rules whenever it wants. So, for value creation in a well-populated ecosystem where no one controls the network, consider a public blockchain.

2. The best option might not be the best technology

There are many different public blockchains to choose from, including Bitcoin, for its value as digital gold, and Ethereum, which has more developers than all the others.

In the same way you can always find a better PC and mobile OS than the ones you're using now, and better networking technologies than the internet, there will always be better blockchains, depending on the measurement criteria. Stop looking for the best one. None of that matters, because in this scenario, the best is relative. The systems with the most developers and users always win. If you want to build practical applications that create value, do it on the network that has the most buyers, sellers and investors.

Also, disregard people who tell you Ethereum is congested. They are the same people who say nobody goes to Venice anymore because it's too crowded.

For a successful blockchain implementation, use public blockchains and connect multiple external parties.

3. Think in native blockchain technology terms

Similar to how companies have business processes, blockchains have tokens and smart contracts. The most successful blockchain implementations are where companies translate their legacy vision into blockchain-native concepts. This means that instead of moving documents back and forth, they shift their thinking to smart contracts and tokenization.

To illustrate this concept, think about something like a purchase order for widgets. We can think of it as a document, or we can think of it as an agreement to buy a certain number of widgets at a specific price. We can pass the information back and forth between the buyer and the seller as participants on the blockchain, or we can create a smart contract that involves exchanging widget tokens for money tokens. This has the same effect and can sound similar, but they are in fact two different worlds. Documents are worthless on the blockchains. Tokens, on the other hand, can be bought, sold, financed and borrowed against.

Sending documents back and forth fails to make use of one of the key ideas in blockchain -- that we can move value as easily as we move information. To illustrate this point, imagine you're moving documents online. Sending documents back and forth is like having a web server that sends you a picture of a page to read, not the text. They are both readable by people, but the text-based HTML document -- blockchain in this scenario -- is also searchable and indexable and can be found by a search engine. One of these approaches is fundamentally much more useful in the web ecosystem than the other.

4. Fix something that is actually broken

Attempting to fix something that isn't broken creates little ROI and is an ineffective use of time and money when it comes to blockchain implementation.

Successful blockchain projects that create value solve actual problems today rather than just laying a foundation for solving problems in the future. Big-picture visions of problem-solving are nice, but they rarely work out. Instead, repeatedly in the history of technology, we find ourselves building platforms on products that solved one small problem but did it very well.

Because success breeds more success, the best thing you can do is select a new problem that hasn't been fixed by existing technology and build a system to fix it.

5. The best ROI opportunities combine multiple parties and shared business logic

Blockchains are great for integrating business processes between companies because they offer all participants the same set of rules, thanks to their decentralized nature. Unlike other systems, such as electronic data interchange, they allow for information to be shared across multiple parties and to include business logic in that shared process.

Sending documents back and forth fails to make use of one of the key ideas in blockchain -- that we can move value as easily as we move information.

A good example is the process of buying goods, which usually includes a buyer, a seller and a shipper. Shared rules like volume discounts and rebates, as well as scheduled pickups make this an ideal candidate. The system becomes more valuable if you include the concept of allowing a subsidiary or a business partner to buy off the same contract. Now you have logic, such as a volume discount, which must operate at a network level -- across firms -- and not just within a single ERP system.

It rarely makes sense to deploy blockchain inside an enterprise, as engineering systems for a decentralized design are more complex and costly than designing centralized systems. Internally, most companies can usually agree upon enough shared rules to make a centralized system the faster and cheaper option.

Creating actual value is, in fact, much harder than innovation theater. Whatever problem you're trying to solve, there's a good chance that someone clever has already spent a lot of time trying to solve it. I believe that using the five tips above, you can speed up your time to value and simplify the problem. That means focusing on figuring out how blockchains solve something that didn't yield to past approaches. Instead of spending a lot of time trying to find the perfect blockchain network, or doing a proof of concept -- we already know that blockchains work -- focus on creating lasting value.

My teams have come to believe that it's, first and foremost, the points of integration between enterprises that represent the single largest area for value creation. The application of equal rules that blockchain offers, combined with the ability to have shared logic and information across multiple parties, solves a lot of problems that haven't yielded to point-to-point solutions or centralized systems.

As the world shifts from competition between companies on their own to competition between networks of companies and value chains, there is enormous scope for creating value in this new era, and one that isn't served by our legacy approaches. I believe, very simply, that blockchains will create as much value for multi-company ecosystems in the coming years as ERP systems did inside the enterprise in the past.

Paul Brody

About the author: Paul Brody is EY's global blockchain leader. He's responsible for driving blockchain investments and initiatives in EY consulting, tax and audit businesses. The views reflected in this article are the views of the author and don't necessarily reflect the views of the global EY organization or its member firms.

Paul Brody

Paul Brody