Scope 1, 2 and 3 emissions: Differences, with examples

With more companies tracking their carbon footprints, Scope 1, 2 and 3 emissions are under discussion. Discover what each is and the approaches to measure them.

Today's enterprise executives are ramping up their environmental strategies to meet growing stakeholder demands. A foundational aspect of that effort is measuring organizational emissions.

Scope 1, Scope 2 and Scope 3 are categories that organizations can use to classify the greenhouse gas emissions (GHGs) they generate across their value chain. The three emissions scopes are the standard categories that define the origin of an organization's greenhouse gas emissions, gases that trap heat and thereby accelerate global warming and climate change. In addition, a fourth scope category helps organizations understand emissions they can avoid.

This guide provides a high-level overview of the following:

- Definitions and examples of Scope 1, Scope 2, Scope 3 and Scope 4.

- A snapshot of calculation methods.

- Challenges of calculating emissions.

- Common carbon accounting tools.

What are the different scopes, with examples?

The organization for global emissions standards, the Greenhouse Gas Protocol, established the scopes of emissions. These are meant to give organizations a framework to measure and report where and to what extent various organizational activities generate greenhouse gas emissions.

Making sense of GHGs

The language of climate change can be difficult to understand. Here's a cheat sheet of some of the important terms related to scopes of emissions.

Greenhouse gas emissions, or GHGs, are the climate-warming gases that trap heat in the Earth's atmosphere and act as a magnifier for the sun. Many scientists agree that human activities, especially burning fossil fuels, are responsible for global warming and climate change. Greenhouse gas emissions are the broadest emissions category. It includes carbon dioxide, methane, nitrous oxide and fluorinated gases.

Carbon dioxide, or CO2, is a colorless, odorless gas that forms most greenhouse gas emissions, which is why many people refer to GHGs as carbon pollution or carbon emissions.

CO2 equivalent is another term associated with emissions: It compares greenhouse gases based on their global warming potential.

Here's a breakdown of each scope.

Scope 1

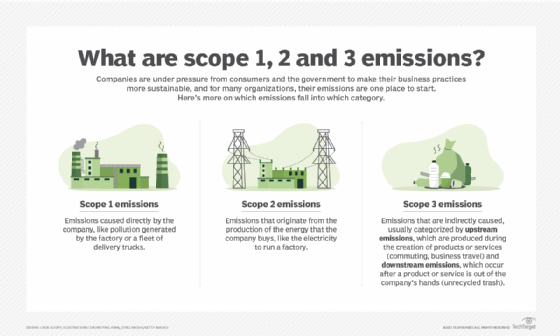

Scope 1 emissions are greenhouse gas emissions that a reporting company generates using its assets. These assets are within the company's scope of control, in other words, the things the company owns or directly controls, which is why Scope 1 is referred to as "direct emissions."

Examples of Scope 1 emissions sources include the following:

- Building furnaces.

- Onsite manufacturing equipment.

- Gas-powered vehicles, including forklifts, delivery vans and other company-related mobile equipment.

- Refrigerants used for commercial cooling equipment, refrigerators and air conditioning systems.

- Accidental leaks and spills, such as refrigerant leaks and chemical spills.

- Fugitive emissions, which are unintentional emissions from things such as industrial processes, refrigerators or gas transmission lines.

- Any controlled or owned asset fuel burning.

Since Scope 1 emissions are within a company's control, it's a natural starting point for setting and accelerating sustainability goals.

Scope 2

Scope 2 includes emissions a reporting organization creates indirectly when purchasing electricity, steam, heat or cooling to run its operations. Scope 2 emissions are considered "indirect emissions" because although the reporting organization's activities generate greenhouse gas emissions, they occur at another source, such as at an energy company's site.

Examples of Scope 2 emissions sources include the following:

- Lighting in offices.

- Electricity for powering machinery or vehicles.

- Natural gas heating for buildings.

- Power for data centers and computing servers.

Although indirect, Scope 2 emissions present both a major source of organizational emissions and a major opportunity for improved sustainability when companies reduce energy consumption or turn to low-carbon resources such as solar energy, wind power or nuclear energy.

For example, CIOs and other IT leaders can improve operational efficiency and choose greener energy sources for enterprise technology systems, including data centers, as a means of reducing Scope 2 emissions.

Scope 3

Scope 3 emissions encompass all other emissions resulting from an organization's operations that aren't part of Scope 1 and Scope 2. As such, Scope 3 comprises emissions produced by entities up and down the organization's value chain, from the raw materials it sources to the disposal of its products. This category of indirect emissions makes up most of an organization's carbon footprint.

Scope 3 can account for as much as 95% of a company's emissions, according to "Tackling the Scope 3 challenge," published by PWC on September 8, 2022.

This category is also more complex than Scope 1 and 2, as it has two subsets: Upstream Scope 3 emissions and downstream Scope 3 emissions.

Upstream Scope 3 emissions

Upstream emissions come from activities in the supply chain that are tied to producing the organization's products and services. Business travel and employee commuting also fall into this category.

This subset of Scope 3 greenhouse gas emissions comprises heat-trapping gases originating from everything needed to produce an organization's products and services. For a clothing manufacturer, upstream Scope 3 emissions would include the GHGs from the production of the fabric it uses to make its clothes as well as the GHGs produced while transporting raw materials from production facilities to the organization's factories. Similarly, a restaurant chain's Scope 3 emissions would include emissions generated in the growing, harvesting and transporting of the food it uses as well as emissions produced in the production, transporting and cleaning of its table linens. Likewise, a logistics company would count the emissions from manufacturing and servicing its vehicles.

Here are the upstream Scope 3 emissions categories, according to "Scope 3 frequently asked questions," published by the GHG Protocol in June 2022:

- Purchased goods and services.

- Capital goods.

- Fuel and energy activities that are not part of Scope 1 or Scope 2.

- Upstream logistics.

- Operationally generated waste.

- Travel for business.

- Employee commuting.

- Upstream leased assets.

Downstream Scope 3 emissions

Downstream emissions arise from activities related to the use and eventual disposal of the organization's products and services, as well as activities associated with operations.

Using the same types of companies highlighted in upstream Scope 3 emissions as examples: A clothing manufacturer's downstream Scope 3 emissions would include climate-warming gases produced in transporting finished products to retail stores and then ultimately to customers wearing and disposing the clothes. Downstream Scope 3 emissions would also include greenhouse gases associated with the product's end-of-life recycling or disposal in landfills. The restaurant chain's downstream emissions would similarly include those associated with composting or disposing of food waste. And the logistics company would count the emissions from reselling, warehousing or disposing of its vehicles when no longer needed.

Here are the categories, also according to "Scope 3 frequently asked questions":

- Downstream logistics.

- Solid product processing.

- Use of sold products.

- End-of-life treatment of sold products.

- Downstream leased assets.

- Franchises.

- Investments.

Scope 4 emissions

Scope 4 is a category the World Resources Institute devised in 2013 to account for what it terms avoided emissions. Many organizations now use this voluntary metric to gain a more detailed understanding of how their direct and indirect activities impact their overall carbon footprints.

Scope 4 comprises emission reductions that "occur outside a product's lifecycle or value chain but as a result of the use of that product," according to "Do We Need a Standard to Calculate 'Avoided Emissions'?" published November 5, 2013, by the World Resources Institute, which established the GHG Protocol.

Some refer to Scope 4 emissions as "climate-positive" or "net-positive" emissions.

According to the World Resources Institute, Scope 4 emissions include low-temperature detergents, fuel-saving tires, energy-efficient ball bearings and teleconferencing services because they have sustainability-generating features. For example, low-energy detergents help avoid emissions from heating water for warm or hot washes. As another example, employees working from home or attending a virtual conference instead of flying to a conference avoid emissions associated with car commuting and air travel, respectively.

How are the scopes calculated?

Calculating and reporting emissions is a complex, multistep process that requires organizations to identify all their emissions sources in each scope first. Organizations can then use formulas, frameworks and tools to collect and analyze the requisite data as well as calculate and report the final figures.

Corporate, sustainability and IT leaders generally require a way to track their emissions over time to understand if they're reaching their sustainability goals or need to step up sustainability activities to hit their desired or mandatory targets.

Similarly, leaders typically need a way to benchmark their emission figures against others in their industry or the overall marketplace to identify whether their sustainability record puts them ahead or behind others and, thus, whether their sustainability record is a differentiator or a liability to them.

Given the complexity of the task, organizational leaders use a combination of protocols, best practices, frameworks, assessment guidelines and software to calculate emissions.

The Greenhouse Gas Protocol has a widely used collection of comprehensive information on calculating emissions.

Calculating Scope 1

Calculating Scope 1 emissions requires assessing emission sources and then using one of two methods to determine emissions: direct measurement via monitoring concentration and flow rates, or the fuel analysis method based on the purchased quantities of commercial fuels and associated emission factors.

Calculating Scope 2

Organizations typically use metered consumption and supplier-provide emissions data to calculate Scope 2 emissions. The GHG Protocol requires organizations to use market-based and location-based reporting methods to calculate and disclose Scope 2 emissions.

Calculating Scope 3

The GHG Protocol publishes its standard and a guide for organizations to complete their Scope 3 inventories. Calculating Scope 3 emissions is the most complex of the categories due to the numerous emissions sources covered by Scope 3.

Calculating Scope 4

Although not as wide-reaching as Scope 3 calculations, Scope 4 calculations are usually more complex than determining Scope 1 and Scope 2 emissions. Scope 4 requires calculating an organizational baseline from which to determine avoided emissions, which includes lifecycle and market assessments, monitoring and calculation methodologies. Although not yet as widely used as other scopes, Scope 4 can help organizational leaders set sustainability goals and determine which suppliers to work with.

Challenges in calculating emissions

An increasing number of organizations are calculating and reporting their greenhouse gas emissions in keeping with various ESG reporting frameworks. Despite such frameworks and emerging legislation, many organizations struggle with calculating their emissions and understanding their carbon footprints.

The "Sustainability action report: Survey findings on ESG disclosure and preparedness," released in July 2024 by professional services firm Deloitte, discusses these challenges.

These are some of the findings:

- 74% of respondents are reporting on Scope 1 GHG emissions, up from 61% in December 2022.

- 53% are reporting on Scope 2 GHG emissions, down from 76% in December 2022.

- Only 15% are reporting Scope 3 emissions.

The survey also found that 57% of surveyed executives viewed data quality as the top ESG data challenge for their companies and 88% reported it as one of the top three challenges for their companies. The availability of and access to quality data is a top challenge in calculating emissions, particularly for Scope 3.

Other challenges include the following:

- Issues with regulations and disclosure standards, which can vary and continue to evolve, have made calculating and reporting somewhat of a moving target.

- Low or limited stakeholder engagement, as not all organizations are required or see the need to calculate and report on GHG emissions.

- Limited resources for sustainability activities and reporting, particularly if reporting is not required.

- Limited experience with and integration of emissions data capturing, tracking and reporting.

Technology tools for carbon accounting and emissions reporting

The dangerous level of climate-warming emissions, and the subsequent pressure to track and report on GHGs and increased scrutiny of the business sector's carbon footprint and overall environmental impact have boosted an interest in carbon accounting software.

The global carbon accounting software market size at $16.92 billion in 2023 and is predicted to grow at a compound annual growth rate of 22.1% from 2024 to 2030, to hit $67.58 billion that year, according to "Carbon Accounting Software Market Size, Share Report 2030," published by Grand View Research.

Grand View Research identified key carbon accounting software providers as the following:

- Diligent Corporation

- Greenly

- IBM

- Microsoft

- Net0

- Persefoni AI

- SINAI Technologies

- Salesforce

- SAP

- Sphera

The research firm noted that growing global awareness and regulatory pressure to reduce carbon emissions and address climate change drive market growth.

More companies taking climate action

As the world grows hotter due to global warming, more business, sustainability and IT leaders are taking action. That action starts with understanding their organization's contribution to the problem so they can begin a sustainability journey.

Mary K. Pratt is an award-winning freelance journalist with a focus on covering enterprise IT and cybersecurity management.